IUL

IUL Calculator – Estimate Tax-Free Income from Indexed Universal Life Insurance

How do you know how much income an IUL will generate for you during retirement? It all starts by using our free IUL calculator on

How do you know how much income an IUL will generate for you during retirement? It all starts by using our free IUL calculator on

Have you ever stopped to wonder if all that money you’re putting into your 401k is really the best thing you can do to make

Are you looking for life insurance? Compare life insurance types and policies to find the right fit. You can choose from several different types of

Retirement accounts come in many different shapes and sizes, each with its unique benefits. One type of account that has gained popularity recently is the

Jim Harbaugh, head football coach at the University of Michigan, is one of the highest-paid college football coach thanks to an innovative compensation package negotiated

Using infinite banking for real estate purchases is becoming more common since mortgage interest rates have soared over the last couple of years. When it

How do you know who the best IUL companies are? There are a lot of IUL companies available to choose from. Making sure you pick

Simply put, CVAT is the acronym for Cash Value Accumulation Test, and GPT is the acronym for Guideline Premium Test. Both of these acronyms have

If you are considering using whole life insurance for lifetime coverage, or to use as a retirement plan, there are some things you need to

You are interested in becoming your own banker using whole life insurance, but you don’t know where to start. Choosing the best whole life company

The rise of federal debt and the likelihood of a high future tax bracket means that people need to take advantage of tax-free income for

Are you considering using the 72t rule to take early withdrawals from your qualified retirement plan to avoid the 10% IRS penalty? As you regularly

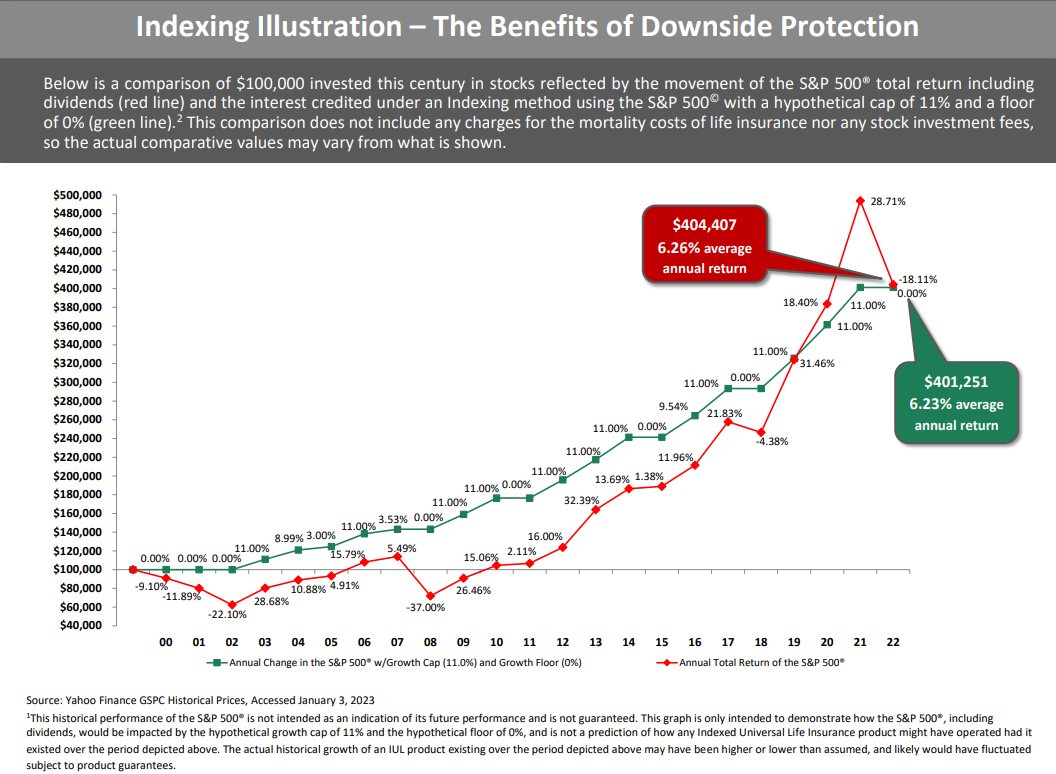

Would it be important to you if after having a terrible year with your investments, that you could, with one stroke, replace all of your

Introduction to LIRP LIRP stands for life insurance retirement plan. The most used life insurance product for a LIRP is indexed universal life (IUL) insurance.

Indexed Universal Life Insurance (IUL) is gaining in popularity year after year because this unique life insurance product provides an affordable death benefit that is

Indexed universal life insurance (IUL) is a permanent life insurance policy that offers a death benefit. Like other types of permanent insurance, your periodic premiums

One of the most important features of any type of life insurance policy is that the death benefit is typically paid to the beneficiary tax-exempt.

The most widespread form of life insurance is for personal use and usually protects a family financially if their loved one dies. Life insurance can

If you’re looking for a type of insurance that offers more freedom and considerable upside potential, you should consider indexed universal life insurance (IUL). This

Borrowing against life insurance is a proven concept that can help you reduce dependence on banks and create a tax-free retirement plan. While this concept

Premium financing life insurance is when a third-party loans you money for life insurance premiums. The lender charges interest and the borrower (the policyowner) typically

Here is our National Life Group review. When searching for the most appropriate and beneficial life insurance policy, it’s important that you find adequate coverage

If you’re looking for a type of life insurance that offers flexibility—as well as the opportunity to have some of the upsides of the stock

Allianz Life Pro+ Advantage Review Established over 115 years ago, Allianz Life Insurance Company of North America has grown its footprint to over 85 million

Due to the recent pandemic, we had seen an increase in seniors over 70 searching for life insurance. Now that the media says we are

Tax-Free Retirement and the Role of Indexed Universal Life (IUL) When I think about retirement, I often picture calm, relaxing days ahead. However, when I

Wondering, “What is a modified whole life insurance policy?” It’s very similar to traditional whole life insurance, but premiums are lower initially. For example, it

In order to understand what paid up additions are on a whole life policy, it’s essential that we first understand what dividends are. Dividends are

Just as the taxes we pay keep our roads paved, life insurance premiums keep us insured and our families protected. No one particularly likes paying

Understanding Whole Life and Guaranteed Universal Life When searching for a life insurance policy, the choice typically comes down to either a permanent insurance policy

Guaranteed Universal Life Insurance (GUL) provides certainty in uncertain times. So, who are the best guaranteed universal life insurance companies? Many people want the assurance

Not all insurance companies operate in the same way. Royal Neighbors of America is a perfect example of that. Instead of simply concentrating on the

If you’re considering applying with Lincoln Heritage, perhaps you’d like to determine if it might be the ideal choice for you and your family? Here’s

Accidental Death Insurance is truly a low-cost alternate choice to life insurance coverage. It is a method for individuals who might normally be declined to

Wow! A $750,000 life insurance policy. This may seem like a lot of life insurance for most folks, but when we really drill down into

Individuals and families who are concerned about what will happen to loved ones if the primary breadwinner dies unexpectedly know that the primary family income

A half-million dollar’s worth of life insurance may seem sufficient for most people, but if you’re trying to replace your income for a spouse and

Aflac offers much more than just entertaining commercials featuring the Aflac duck. Since 1955, Aflac has been providing people with a wide variety of insurance

A $250k whole life Insurance policy can be a great cornerstone for a strong financial plan. Let’s look at a $250k whole life insurance policy

For most people, a $100,000 life insurance policy may sound like legitimate coverage and that may be true. There are circumstances when $100,000 in coverage

Term life insurance is cheap. You might be able to buy $100,000 of term life cheaper than a $50,000 life insurance policy, so make sure

When shopping for life insurance, a lot of people say that the only thing more challenging about life insurance products is the number of companies

Believe it or not, there was a time (the good ole days) when decreasing term insurance was popular. Consumers primarily used it to cover a

Anyone who watches television has probably seen commercials put out there by life insurance companies, especially those companies that sell directly to the consumer. Our

Do you prefer to wait weeks to get your life insurance issued while your insurance company collects health information about you and sometimes your immediate

When you embrace 21st Century technology, you can buy almost anything online. The days of purchasing a product like life or health insurance only from

If you’re in the market for insurance and want to buy it fast, cheap, and from a highly-rated insurance company, Policy Genius is a great

Let’s put first things first. SelectQuote is not an insurance company, but rather an insurance agency. This is a good thing for consumers because it

Certainly, most people have heard of Progressive Auto Insurance because we are regularly greeted by Flo and Jamie who spend a lot of time hawking

Although Return of Premium Life Insurance entered the insurance market with a “Bang,” the interest has begun to wane as many financial gurus condemn the

In our effort to educate our prospective insurance clients, we feel obligated to offer our Colonial Penn Life Insurance review. If you watch any television

American Amicable Insurance Company of Texas is a very unique life insurance company offering a full lineup of life insurance products. We see this company

We know it can be difficult to find a no-exam life insurance for seniors over 75. Life insurance is one of the best purchases that

Organized as a fraternal benefit society, Foresters Life Insurance Company is not your run-of-the-mill life insurance provider. Offering life insurance, annuities, mutual funds, and other

Aside from ensuring that you have the perfect insurance policy to fit your needs, it’s vital that you have enough coverage for you and your

I can’t tell you how often my clients underestimate the importance of their life insurance medical exam and knowing this, we offer the tips to

North American is a top choice for us. They are rated A+ by AM Best and have a Comdex Score of 92. Our full North

Although Ameritas has been around since the late 1800s, many U.S. consumers are unaware of this insurance company and how far they’ve come. Originally established

Life insurance is an integral part of most any complete financial plan. That’s because the proceeds that are received from these financial vehicles can be

Banner Life Insurance Company is also known as Legal and General and they do business in the state of New York as William Penn Life

Many life insurance companies have started offering an IUL retirement account to customers who are risk averse and want to pay less taxes in retirement.

Accumulating wealth for retirement can be stressful and confusing, there’s no doubt about it. Research reveals differing opinions, pros and cons, and scam declarations, with

If you are looking for a life insurance no waiting period and no medical exam policy, you will need to know which companies will give

Whether you own a small, medium, or a large business, in today’s economy finding and keeping the best employees can be difficult. All business owners

If you’ve ever thought about retirement planning or purchased life insurance from a reputable agent or financial planner, chances are that “Life Insurance Trust” may

A Premium Deposit Account (also called a premium deposit fund) was designed for life insurance applicants who want to deposit a lump sum of money

Formerly known as The College Life Insurance Company, Americo Financial Life and Annuity Insurance Company has been established for over a century. This is our

Borrowing the money from a third-party lender to pay for a large life insurance policy is becoming more popular as lenders look to capitalize on

THE VOLATILITY SHIELD How to Vanquish the 4% Rule & Maximize Your Retirement Income A Financial Novella by David McKnight If you are a

If you own anything, you have an estate; plain and simple. It doesn’t matter how valuable your estate is or how modest it may be,

First off, we are not Zander Insurance. This is our Zander insurance review which we consider fair and balanced. Most of the time when we

In the many articles, we have provided regarding Indexed Universal Life Insurance, we have on many occasions mentioned the modified endowment contract but have not

If you think that your Social Security benefits will be sufficient for you to live on in retirement, think again. Regrettably, even if you are

Look Before You LIRP Why All Life Insurance Retirement Plans are Not Created Equal, and How to Find the Right One for You by David

The Power of Zero – How to Get to the 0% Tax Bracket and Transform Your Retirement by David McKnight In the Power of Zero

Most people have a vague idea of how life insurance works but generally they don’t understand the fundamentals of a life insurance contract and how

When we review the numerous Clark Howard life insurance articles, it doesn’t take much reading to discover his take on the subject. It’s interesting that

When most people think of life insurance benefits, they think of providing financial protection for their loved ones or using the cash value as an

Are you looking for an alternative to traditional retirement products? Have you found that when you look at the big picture, your IRA, 401(k), Roth

When we apply for life insurance, there are three primary factors that determine the rate classification: our age at the time of the application, the

Kai-Zen premium financing is a strategy that enables you to supercharge your retirement plan. Kaizen is simply a concept that allows you to finance the

Fixed-indexed annuities are insurance products that offer three guaranteed benefits for investors: Guaranteed principal protection. Guaranteed minimum interest rate. Guaranteed income when choosing to annuitize.

The Protective Life Insurance Company offers a wide variety of life insurance products. Very popular for term life insurance, Protective Life also offers universal life

As American savers become more conservative. There is more interest in saving for retirement in permanent life insurance policies. Permanent policies allow the policy owner

Are you familiar with Roth IRA conversions? An IRA rollover to IUL can also help in saving taxes during retirement. Here is how: Your account

I remember (a long time ago) when I was starting a family and I knew I needed life insurance. I called a friend of mine

Most financial advisors you talk to will stress the importance of planning for retirement. To make sure you have enough retirement savings, you need a

Most consumers know that term insurance is the most affordable life insurance coverage available in the life insurance marketplace. Term Life Insurance has become the

For most people who know even a little about life insurance, most will agree that it seems like whole life insurance has been around forever.

Most people know at least something about term life insurance. They typically understand that term is the cheapest life insurance available and they understand that

Term Life Insurance is considered to be the cheapest life insurance that a person can buy. Because of this, term life insurance is typically the

Most insurance advisors will have knowledge of how a 1035 exchange works. From time to time clients or prospective clients will have a life insurance,

Columbian Mutual Financial Group (CMFG) which is a subsidiary of Columbian Mutual Life has roots that go back more than 130 years now. This financial

Certainly, when considering life insurance for you and your family, premiums will play a major role in your purchase decision. However, price alone should not

The Infinite Banking Concept enables individuals, families, and businesses to develop financial independence by becoming your own banker. This concept was implemented by R. Nelson

If you have recently closed on a home loan, you’ve likely received several notices about mortgage protection insurance. Did you read them or throw them

With Term Life Insurance rates being lower than ever before, there’s no wonder that so many policies are sold today, especially for consumers who need

Beginning in 1911, Washington National Insurance Company has been diligent in protecting families from the financial burden that often accompanies accidents, critical illnesses, and death.

Beginning long ago in 1904, Mutual Trust Life Insurance Company has been providing life insurance policies to U.S. consumers for over a century. During that

As one of the most well-known names in the industry since 1882, The Knights of Columbus was founded by Father Michael J. McGivney in New

Founded in 1840, Sagicor Financial Corporation was originally known as The Barbados Mutual Life Assurance Society. Throughout the latter part of the 1800s, the company

For nearly 140 years, Prudential Financial, Inc, commonly referred to as Pru or Prudential has been maintaining its status as an excellent company offering insurance

As we have mentioned before and will discuss again, a life insurance retirement plan or LIRP is a robust financial planning vehicle used by consumers

For anyone considering a stint or career in the military and worried about life insurance, worry no more. Servicemembers’ Group Life Insurance (SGLI) is a

Shopping for life insurance coverage, specifically indexed universal life insurance, can be a tough decision. When you decide to use IUL for retirement planning, you

On August 29, 1954, the Federal Government sanctioned and established the Federal Employees’ Life Insurance Program which is commonly referred to as FEGLI. Since then,

Permanent life insurance has been devised to last your entire life (lifetime guarantee) and to provide your beneficiary a payout once you die. Unlike term life

We give Transamerica life insurance the green light. They have excellent ratings from AM Best. They have term life insurance, simplified issue whole life insurance

Dealing with most traditional life insurance companies often means complicated paperwork and longer than normal wait times for approval. However, Haven Life Insurance Company expedites

Can I get life insurance if I have Diabetes? There are many myths about diabetes. These myths stand in the way of the facts about

Are you a smokeless tobacco user? We have to life insurance companies that you will find cheap life insurance for chewing tobacco use. Prudential and

Primerica Life Insurance, or Prime America as its often called, is one of the leading providers of term life insurance for millions of consumers. Regarded

Cigar and pipe smokers face an issue in their efforts to select a term insurance policy that will be suitable for their budget. Finding life

Even if you have not had children, chances are that you’ve heard the name Gerber. This large American company is also known to provide life

Even though most individuals don’t like to think about life insurance, the fact is that it’s a very important part of your financial plan. The

The Principal Financial Group is the world’s leading financial service groups. Principal offers both insurance and financial products to businesses and consumers worldwide. They have

A common question asked by most shopping for life insurance is whether AARP is a life insurance provider. The short answer is no, AARP is

United Home Life insurance company is highly regarded in the impaired risk and final expense marketplace. As a matter of fact, diabetics do very well

When purchasing life insurance, there are some important factors to consider, such as the type of policy you desire and the life insurance coverage amount

Purchasing life insurance is one of the most important investments one can make during their lifetime. Equitrust life insurance company with a strong focus on

Mutual of Omaha got its start over a century ago in 1909, and at that time was named Mutual Benefit Health & Accident Association. Within

With the vast amount of life insurance companies available today providing coverage, it can be overwhelming when shopping around for life insurance. An insurance company

Important in everyone’s financial portfolio, life insurance helps to protect loved ones from having to foot the bill for final expenses and other expenses that

Like most insurance products, life insurance is an important product to carry. Despite the fact that most individuals don’t’ want to reflect on their own

Although most people in the U.S. are familiar with AAA Insurance because of their Motor Club, the company is in the life insurance business too.

What would happen if you were diagnosed with a serious medical condition? Would your health care insurance cover all of your expenses? Out-of-pocket medical costs

Nearly every single person has been touched by a critical illness at some point in their lives, either directly or to someone they know. This

At age 39, you can still get very affordable life insurance rates. Term life insurance is still very cheap and it may be a great

Many couples first seriously consider life insurance in their mid-thirties. You are old enough now to know that unexpected tragedy is a reality you want

If you were to be diagnosed with a chronic or critical illness would you have the resources available to make certain that you and your

Did you know that you can buy your life insurance at Costco and get a 20% discount. That is if you are a Costco member.

We rate American General as a solid company with high ratings and ease of doing business. Term life insurance rates from American General are very

We reviewed State Farm and they are a winner. As the slogan goes: Like a good neighbor, State Farm is there. State Farm is one

Should you replace your life insurance policy? Your current term life insurance policy is running out and premiums are increasing You had a baby You

Many of our life insurance companies offer life insurance with no need to complete a medical exam. The amount of life insurance you can get

Are you the kind of consumer who makes decisions based on what family and friends recommend or maybe even television commercials about a product or

Our review of William Penn Life insurance. Only if you live in New York. If you are in any other state you would use their

It makes sense that since Progressive is a major player in the property and casualty insurance market that you can trust them to be a

Just so you know before reading this entire article, Genworth Financial life insurance no longer offers life insurance. They have stated that their focus will

Founded in 1868 by former California Governor Leland Stanford, Pacific Life Insurance Company has grown to a Fortune 500 Company. The company eventually moved their

Have you tried to get a Geico life insurance quote lately? Geico is not just a car insurance company. Certainly, Geico is one of the

As an insurance professional with over 25 years experience in the industry, I often have to chuckle and grin when I come across pages of

For those of you familiar with Dave Ramsey and his opinions about life insurance, you may find it interesting that he’s not licensed to sell

Vaping and e-cigarettes can increase your rates for life insurance if you apply with the wrong company. Although there is no term like vaping life

Indexed Universal Life Insurance – The Most Expensive or the Best? Once you understand what indexed universal life insurance is all about, you will be

There are many reasons why people purchase life insurance. For some, the proceeds are intended for paying off debt and / or for replacing the

Life insurance is one of the best products that you’ll ever purchase for your family, but you may ask the question, should I start an

There are many reasons that you may plan for your death, one being the provision of an income for those that you love so that

Even in this age of online education and wild business success stories told by dropouts who are making millions, nothing can beat a good, well-rounded

Quick fact: Life insurance costs more for smokers. Here is how you can get cheap life insurance for smokers. This includes cigarettes, pipes, cigars, e-cigarettes,

In today’s world, changing jobs is not a monumental undertaking. The concept of staying at one job for 30-years is pretty are. In fact, the

In the retirement planning marketplace, the term life insurance vs IUL indexed universal life insurance debate continues. The proponents of IUL are typically insurance and retirement

Previously on this blog, we’ve touched upon using indexed universal life for some seemingly unconventional purposes such as retirement planning and mortgage protection. One of

If you have people in your life that you care about, then it is likely that you need life insurance. With the proceeds from a

Penn Mutual Life Life insurance has been around for over 175 years and is rated A+ by AM Best. When considering life insurance, you need

Life insurance is a key component of many good, complete financial plans. This is because the proceeds that are received from a life insurance policy

Absolutely! Many people go on to live long and healthy lives after heart valve replacement surgery. The success and reliability of heart valve surgery are

When you apply for life insurance, the company is going to look at dozens of different factors to determine how much they are going to

Wow! How time flies! Seems like just yesterday that the real world would open its doors and say here I am, come and get it. Well, age

I am 50. Should I Buy IUL Insurance? Who should buy IUL insurance? Life insurance is one of the smartest financial decisions you can make

Life insurance is one of the most important purchases that you’ll ever make for your loved ones. It’s one of the only ways that you

Tony and Gwen purchased indexed universal life insurance also known as IUL insurance at age 43, here is why… Tony was 43 years old when

When you’re looking to buy life insurance, it can be a confusing and frustrating process. There are several different types of plans that you’ll need

Many women (and a few men! — more about that later) develop benign breast cancer during their lives. The Emory Healthcare website states that “although

When you apply for life insurance coverage, there are dozens of different factors that the insurance company is going to review. They are going to

Do you suffer from health problems and feel that life insurance at 70 will be too expensive to afford? What you may not understand is

Shopping for life insurance can be difficult, especially if you have a serious pre-existing condition. If you want abdominal aortic aneurysm life insurance, you may

When you’re applying for life insurance, the company is going to look at dozens of different factors to determine if they are going to accept

Finding the best life insurance with asthma can be difficult. If asthma is treated properly and not ignored, underwriting will be easier on you. On

How to Find Affordable Life Insurance After a Stroke Many people who have had a stroke worry that they can no longer buy life insurance.

You have the life insurance you and your family need. Your policy is in place and whatever happens to you, your loved ones will always

Where is the cheapest place to buy IUL? I get this question from time to time when working with my clients. The answer may surprise

Life insurance is one of the best safety nets that you could ever buy for your family. It’s one of the only ways that you

If I was 45 years old, would I buy IUL? You bet I would. Fortunately, I started buying permanent life insurance when I was 25

Burial insurance is a popular form of life insurance coverage that is a great way for applicants to provide coverage, even if something tragic were

If you’ve ever been declined for life insurance in the past, then you should consider getting a whole life insurance no medical exam policy. There

When I started in the life insurance business in 1995, new agents that came into the insurance business worked for one company. These companies were

When I was in my early twenties, with two young children at home, a good friend of mine was diagnosed with terminal cancer. He had

If you or someone you loves has diabetes, you are not alone. According to the American Diabetes Association, in 2012, 29.1 million Americans had this

Earning your pilot’s license is a thrilling experience. Some people decide to get their aviation license to help with a long commute or for agricultural

A lot of kids dream of being a pilot when they grow up. Who wouldn’t want to hit the skies? Being a pilot brings a

Can I Get Life Insurance With High Cholesterol? It is estimated that over 70 million Americans have high cholesterol and only one in three

Term life insurance can be one of the best safety nets that you can purchase for your loved ones. It’s one of the only ways

Prostate cancer is the number two most common cancer in American men, behind skin cancer. It is estimated that one in seven men will be

Although mitral valve prolapse (MVP) is associated with some serious health complications, the incidence of these problems is minimal. Most people who have MVP experience

Here at Ogletree Financial, we get a lot of questions every year. Some of them are easy to answer, while others are a bit more

Announcing the unfortunate passing of musician Glenn Frey, the Eagles website states that “Glenn fought a courageous battle for the past several weeks but, sadly,

When you’re looking to get life insurance, there are dozens of different factors that you’ll have to consider to ensure that you’re getting the best

Life insurance is one of the most important safety nets that you could ever purchase for your family. It’s one of the only ways that

When you apply for a life insurance policy, the insurance company is going to review a variety of different factors when looking at your application.

Life insurance is one of the most important purchases that you’ll ever make for the future of your family. It’s one of the few ways

Life insurance is one of the single most important purchases that you’ll ever make for your loved ones. It’s one of the only ways that

Life insurance at 79 is probably not as uncommon as you think, or as expensive as you think. If you have important financial obligations, a

It’s no too late. The premiums will not be as high as you think and your health issues will not matter as much as you

Cheap life insurance with high blood pressure? Absolutely! We often get standard and even preferred and preferred plus risk ratings for clients with high blood